MoneyLion

Instacash®

Here’s what to know

Get fast cashTap into your pay whenever you need it. You have the reins.

Get fast cashTap into your pay whenever you need it. You have the reins. No strings attachedNo interest. No credit check. No mandatory fees.

No strings attachedNo interest. No credit check. No mandatory fees. Instant accessAccess your pay fee-free within 1-5 business days or instantly for an optional fee.1

Instant accessAccess your pay fee-free within 1-5 business days or instantly for an optional fee.1

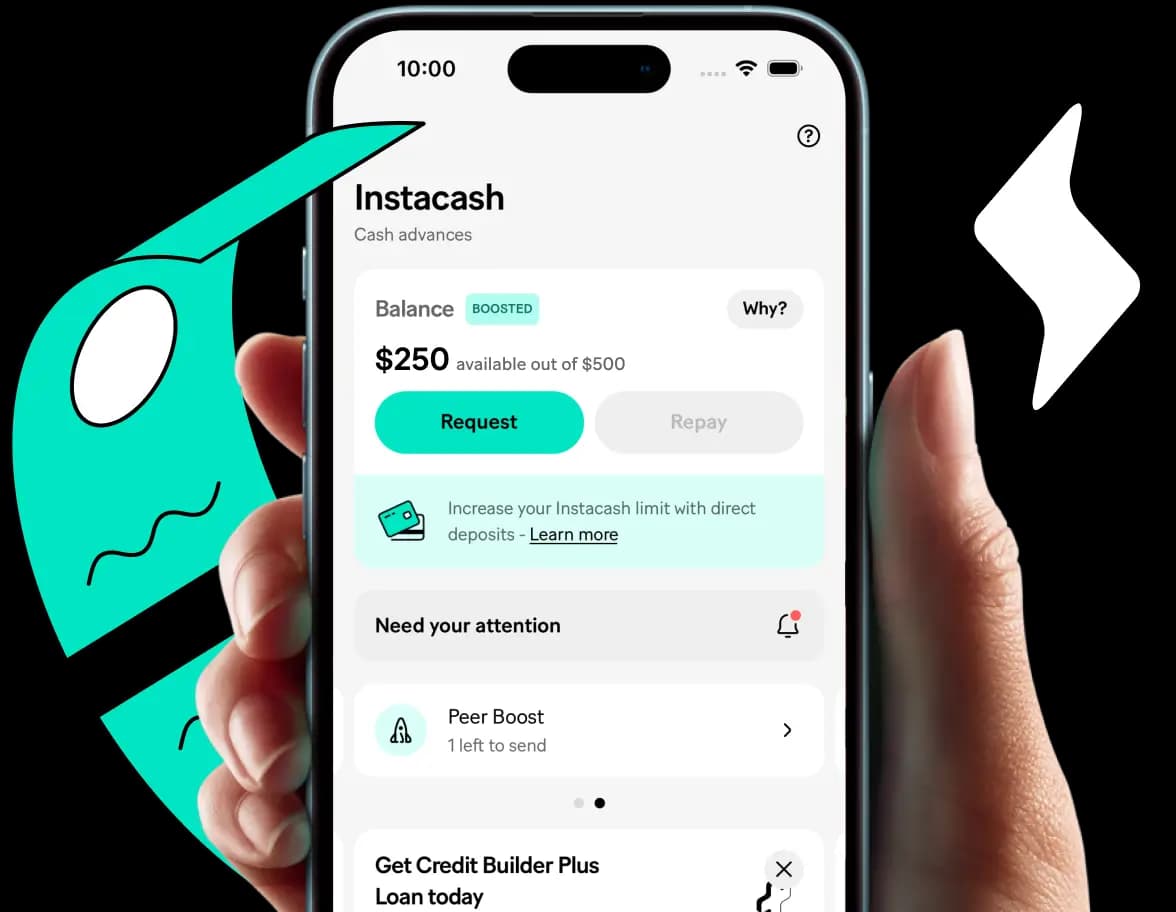

Get up to $500. Fast

Need More?

No Stress,

No Hassle.

How does it work? Simple.

- Link the bank account where you receive your paycheck to see if you qualify.

- Select the amount you want.

- Confirm, and voila! You're done. Enjoy your cash.

93%

of Instacash customers have felt more in control of their finances since they started using Instacash.88%

of Instacash customers believe Instacash is their best option when they need access to cash.89%

of Instacash customers believe they are better able to take care of themselves and their dependents since they started using Instacash.

- This app was a total life saver. I put myself in a terrible situation right before payday and was able to access funds immediately and now.Melio07 from App Store7/27/23

- They are the best when you are in need of fast cash.Cobra12King Adams from Google Play7/12/23

- MoneyLion is the best cash advance app that I’ve used. The app is very user friendly, and they will work with you as long as you communicate with them. If I ever need a cash advance again, I’m definitely going through Moneylion!ERJr@3232 from App Store7/27/23

Never Overpay For Fast Cash.

Learn more about Instacash

You've got questions. We have answers.

To apply for cash advances up to $500, tap Instacash on the Home screen of the MoneyLion app. You’ll find out right away how much you can get. There’s no interest, no monthly fee, and no credit check! Here’s more info on qualifying.

It’s easy to increase your available Instacash amount by setting up direct deposits into a MoneyLion Spend account. You’ll unlock cash advances up to $1,000** depending on your qualifying income.

HOW TO USE INSTACASH

- Download the MoneyLion app if you don’t have it.

- Open the app, go to the Finances tab.

- Tap the Instacash button at the top.

- Tap the Request button

- Select the amount you want, and how soon you would like the funds transferred to your account. Note: there is a maximum of $100 per disbursement.

- When you use Instacash, the amount you’ve taken out is automatically deducted from your account on the repayment date as determined by your pay cycle – with no interest. You can take another Instacash once you repay your last Instacash as long as you maintain your eligibility.

To unlock 0% APR Instacash advance, tap the Instacash button on the Home Screen. All you need to do is link your checking account to apply. It’s secure and quick. We’ll then verify your checking account and your identity so you can get cash quickly.

CHECKING ACCOUNT MINIMUM REQUIREMENTS

We’ll review your linked account to confirm that it meets or exceeds our minimum qualification requirements. You can improve your chances of qualifying by linking a checking account that meets or exceeds the following criteria:

- It’s not too new: Choose an account that’s been open for at least two months.

- It shows income deposits: Pick the account where you regularly deposit your income/paychecks and have a history of depositing income.

- It has a positive balance: Choose an account where you have consistently maintained a positive balance.

- It’s active: Choose an account that you have used and continue to use regularly!

Any account that cannot be confirmed as a checking account, such as a savings or money market account, will not qualify for Instacash.

IDENTITY VERIFICATION REQUIREMENTS:

We must be able to verify your identity and checking account ownership:

- Enter your info as it appears on your bank account. We’ll check the info you enter against the details we receive from your linked bank to make sure they match.

- Make sure your info matches your public records. We’ll also check the info you enter against electronic public records.

If your account doesn’t qualify, please try again when it has been open longer and/or had more consistent deposits and positive balance — or try another checking account!

Please note: If you’re a Credit Builder Plus member but you have late or missed loan payments, you may not be eligible to take out Instacash advances until your account is in good standing.

No! We don’t do any sort of credit pull or credit check during or after an Instacash request.

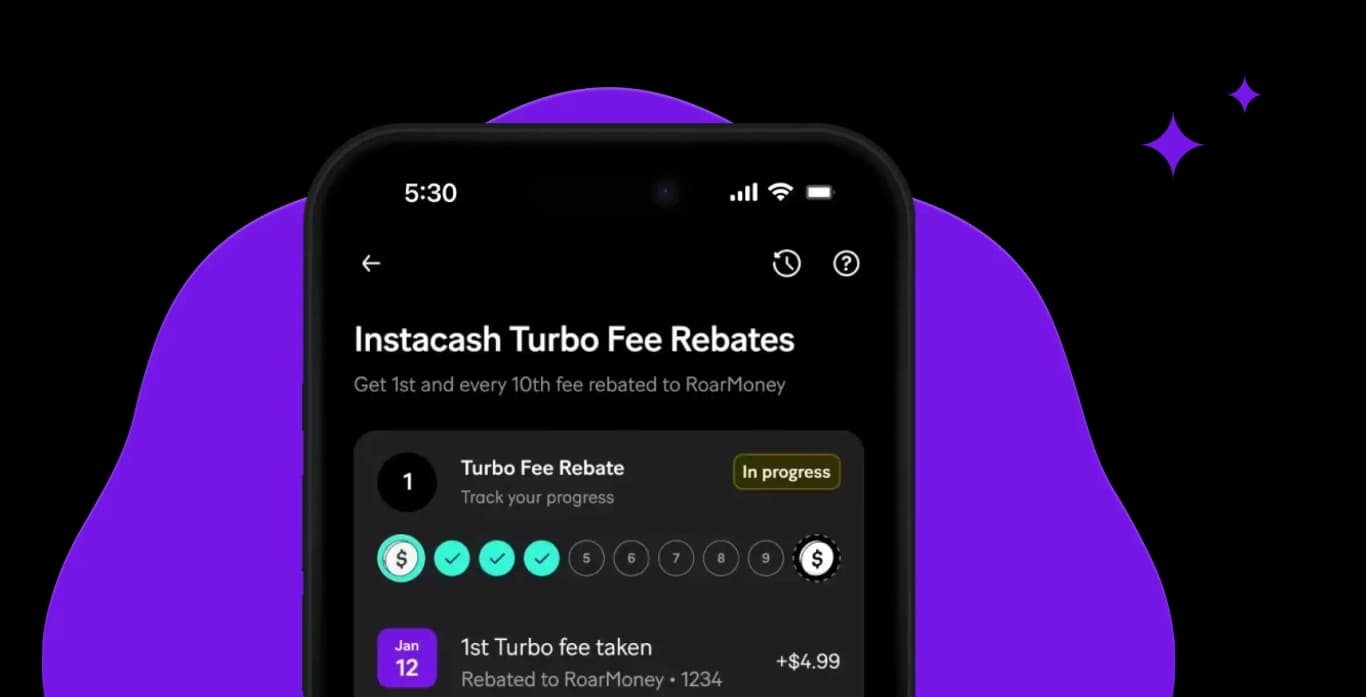

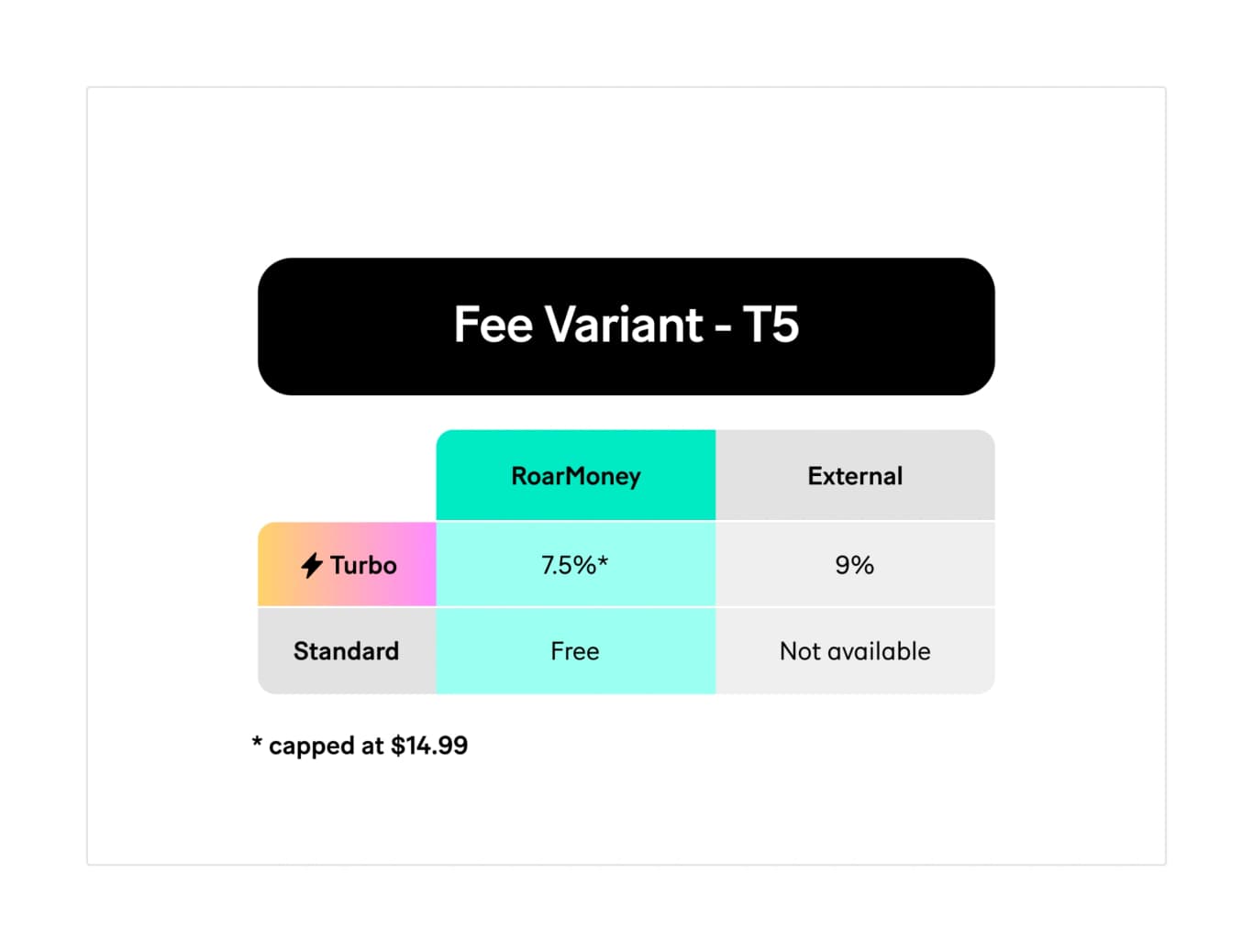

You can unlock Instacash for free! Standard delivery (which could take up to 5 business days*) for no cost or you can choose the optional Turbo delivery and get your cash within minutes. Turbo delivery fees vary. There’s no monthly fee and no interest. Any Turbo fees and tips are totally optional. Whether you choose to tip and/or pay a Turbo fee for expedited delivery does NOT impact your access to Instacash or your Instacash limit.

Each time you get an Instacash advance, you can select from these disbursement options, some of which have associated costs:

- Regular delivery (1 – 2 business days*) to your MoneyLion Spend** account – $0

- Regular delivery (2 – 5 business days*) to your external checking account – $0

- Optional Turbo delivery (within minutes) to your external debit card or eligible external checking account or MoneyLion Spend account – refer to the fee table below:

Lastly, every time you take an interest-free cash advance, you will have a choice to leave a small optional tip in appreciation of the Instacash advance service.

Instacash repayments are automated, making it easy to pay on your scheduled repayment date and replenish your Instacash so it’s ready when you need it next! On each scheduled repayment date, the amount of Instacash you received and any related optional Tips and optional Turbo Fees will be automatically deducted from your authorized payment account or debit card. There’s no interest charged.

Here’s how automated Instacash repayments work:

- When you request an Instacash advance, you authorize us to electronically debit your MoneyLion Spend account, a third-party debit card, or an external linked checking or spending account on the scheduled repayment date. If there is not enough balance in your account, we may deduct a partial repayment and make additional debit attempts until the Instacash amounts are fully repaid (subject to your right to withdraw the payment authorization for your payment methods).

- If repayment from the payment methods stated above is not successful, we may attempt a debit on any additional payment methods you have added to your ML Wallet.

Head here to learn more about Instacash repayments.

After you unlock Instacash, if we can detect qualifying recurring direct deposits in your linked checking account and can predict when your income is deposited into your account, you’ll have access to Instacash limit of up to $500. Typically, higher deposit amounts will unlock higher Instacash limits.

You can increase your Instacash limit up to a maximum of $1000** (depending on the anticipated income amount) by switching your direct deposits into a MoneyLion Spend account. It’s easy to do this in the app at anytime or through your employer or other payor. Learn more on how to do so here.

Alternatively, you can sign up for a paid MoneyLion membership, which can also increase your Instacash limit up to $700.

If you are not currently eligible for our complete Instacash experience, you may be eligible for our Trial experience, which allows you to start with a minimum of $10 and unlocks higher limits by advancing through a repayment progression program. See here for more information about Trial Instacash.